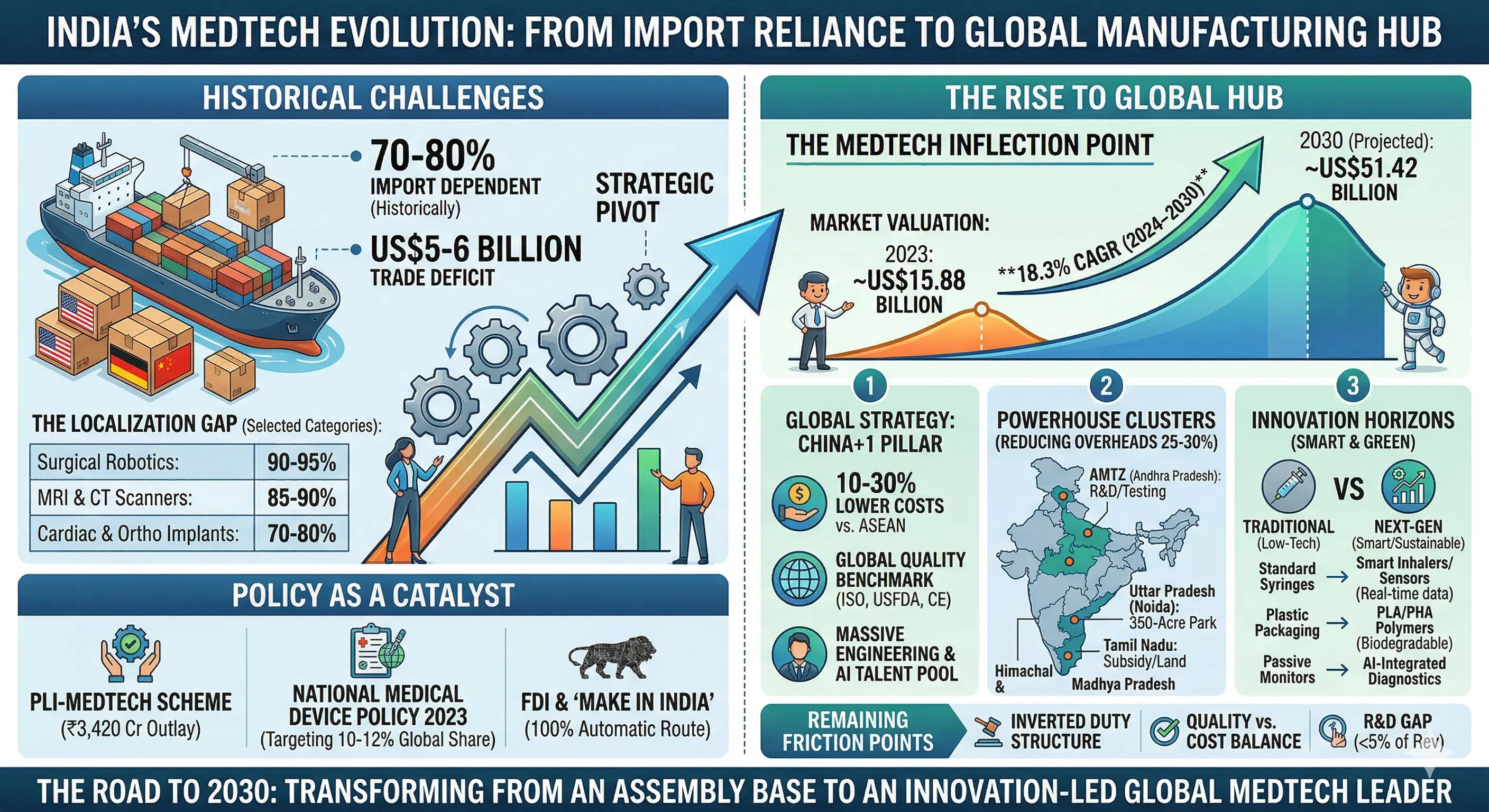

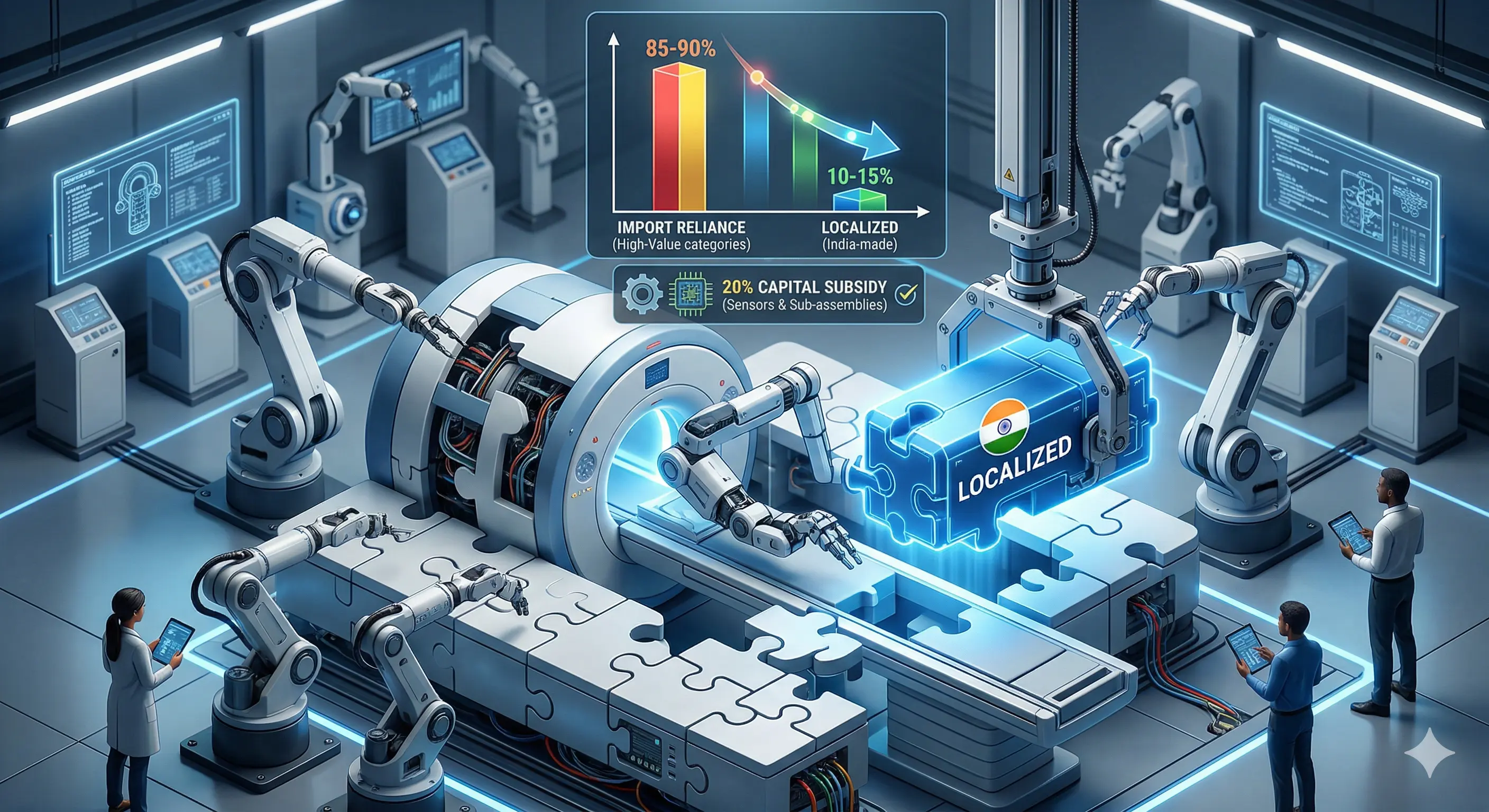

2. Decoding the "Import Dependence" Challenge

Historically, India has been 70–80% import-dependent, particularly in high-precision, capital-intensive technology. While domestic firms command 65% of the market in low-tech consumables, the "Localization Gap" remains widest in life-saving diagnostic and surgical categories.

Synthesis: The Economic Multiplier Localization is more than a healthcare imperative; it is an industrial engine. Moving toward domestic production triggers a "multiplier impact" across the engineering and MSME sectors. To facilitate this, the government has proposed a 20% capital subsidy for the production of key MedTech components, encouraging backward integration into sensors and precision sub-assemblies.

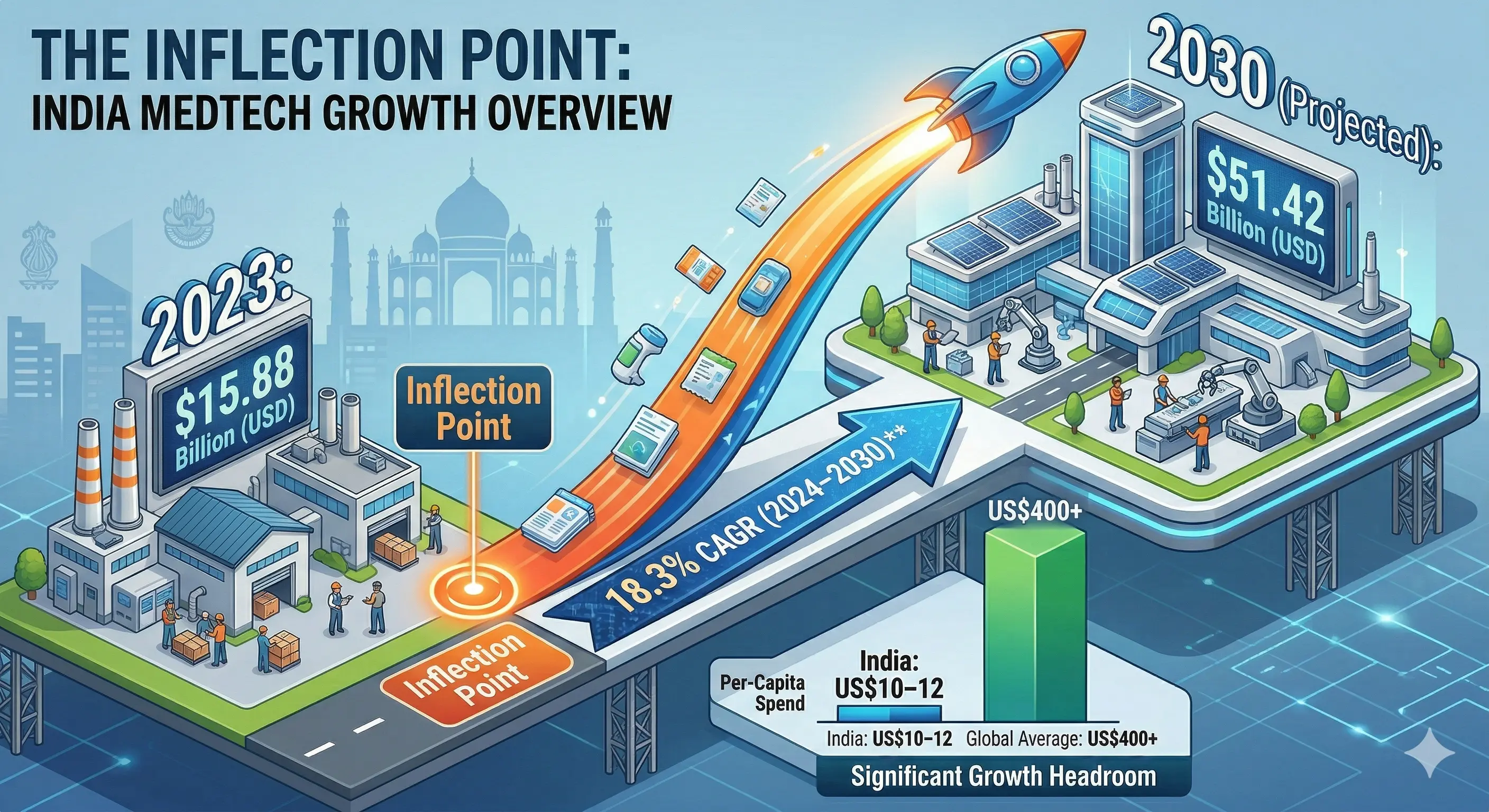

Transition: As global players seek to mitigate supply chain risks, this localization effort aligns perfectly with the shifting global geopolitical landscape.

--------------------------------------------------------------------------------

3. The "China+1" Strategy and India's Global Pivot

The global MedTech industry is currently undergoing a structural realignment characterized by the "China+1" strategy. Multinational corporations are diversifying their manufacturing bases to reduce single-source dependencies, driven by two overlapping forces: geopolitical trade risks and the need to serve burgeoning regional demand in South Asia.

India is positioning itself as a "Trusted Value Manufacturer" through:

- Cost Advantage: Manufacturing costs in India are 10–30% lower than those in ASEAN hubs due to labor and operational efficiencies.

- Regulatory Alignment: Adoption of international standards (ISO, USFDA, CE) is turning "Made in India" into a global quality benchmark.

- Engineering Talent: A massive pool of talent in electronics and automation supports the scaling of precision production.

Learning Insight: India’s role is evolving from a mere consumer market into a "quality-compliant alternative" that offers global supply chain resilience without compromising on clinical standards.

Transition: This strategic pivot is anchored in the development of specialized physical infrastructure across the country.

--------------------------------------------------------------------------------

4. Powerhouse Clusters: The Engine of Regional Manufacturing

To lower the cost of entry for manufacturers, India has established dedicated clusters that reduce production overheads by 25–30%.

- Andhra Pradesh MedTech Zone (AMTZ): India’s largest integrated cluster, hosting an IIHMR satellite center for talent and providing shared testing labs that reduce upfront R&D costs for startups.

- Uttar Pradesh: Home to the Noida Medical Device Park, a massive 350-acre development designed to host high-value manufacturing units.

- Tamil Nadu: One of the four government-approved parks, offering 25–50% capex subsidies and land incentives to attract global OEMs.

- Himachal Pradesh & Madhya Pradesh: The remaining two approved parks, specifically designed to provide shared infrastructure and SGST reimbursements to streamline the "Make in India" agenda.

Transition: These clusters are not just producing traditional supplies; they are the breeding grounds for a new generation of "active" and "smart" technologies.

--------------------------------------------------------------------------------

5. Innovation Horizons: Smart, Green, and Automated

The industry is transitioning from high-volume "passive" products to high-value "intelligent" devices. Diagnostic and Laboratory Disposables have emerged as the most lucrative and fastest-growing segment as diagnostic chains expand into Tier-II and Tier-III cities.

Learning Insight: The shift to SMMS fabric (Spunbond/Meltblown) is a strategic response to evolving procurement models. Hospitals now integrate sustainability into tender processes, making green materials a business necessity rather than an elective choice.

Transition: This wave of innovation is being accelerated by a series of aggressive government policy levers.

--------------------------------------------------------------------------------

6. Policy as a Catalyst: PLI and the 2023 National Policy

The regulatory environment has shifted from a restrictive framework to a proactive facilitator through three primary levers:

- PLI-MedTech Scheme: A ₹3,420 crore outlay offering a 5% incentive on incremental sales, specifically targeting the domestic manufacture of high-end devices.

- National Medical Device Policy 2023: A comprehensive roadmap designed to streamline approvals and boost India’s global market share from 1.5% to 10-12%.

- FDI & "Make in India": Allowing 100% FDI under the automatic route has led to massive capital inflows, such as Medtronic’s US$350 million R&D expansion in Hyderabad.

Transition: However, these incentives face significant structural bottlenecks that threaten to derail the 2030 vision if not addressed.

--------------------------------------------------------------------------------

7. Navigating the Friction: Structural Bottlenecks

- Inverted Duty Structure: A primary friction point where the tax on raw materials (like specialty polymers) is higher than that on finished imported goods, effectively penalizing local manufacturers.

- Quality vs. Cost: Manufacturers must navigate the extreme price sensitivity of the Indian market while bearing the high costs of international safety certifications (ISO, USFDA).

- Electronic Component Dependence: India remains vulnerable to supply shocks, importing 70–85% of critical electronics like semiconductors and imaging tubes.

- The R&D Gap: Indigenous R&D investment remains at <5% of revenue, trailing far behind the global average of 8–10%, leading to fewer domestic patents.

Learning Insight: Addressing these bottlenecks is essential to curbing the trade deficit, which otherwise continues to inflate hospital CapEx and limit healthcare affordability for the end patient.

Transition: Despite these hurdles, the roadmap to 2030 reveals an industry on the brink of global leadership.

.svg)